According to a new study commissioned by the Texas Solar Energy Society and produced by Dunsky Energy and Climate Advisors, the value of solar (VOS) is experiencing externalities.

Externalities, according to the International Monetary Fund, are a market failure that occurs when a good’s “indirect effects have an impact on the consumption and production opportunities of others, but the price of the product does not take those externalities into account.” Put simply, it’s when a good’s price doesn’t reflect its true value.

Externalities are either negative (when a cost is not reflected in the price) or positive (when a benefit is not reflected in the price). Both positive and negative externalities result in market inefficiencies. If the externality is negative, producers overproduce the good (shifting unaccounted costs to consumers), and if positive, producers underproduce the good (shifting unaccounted for benefits to consumers).

In Texas, solar displays positive externalities. Distributed solar producers aren’t being paid for the full dollar value of the kWh(s) they put out, so Texas produces less solar than we could/should be. It’s unclear what the full impact of the externality is on the state’s economy, but we have approximated the difference between what solar owners are paid, and what they should be paid.

First, some background on the Dunsky-commissioned study. Dunsky estimated the “distributed solar PV’s generation, delivery, and societal value across the Deregulated market within the Electric Reliability Council of Texas (ERCOT) territory”. Basing their study on a set of assumptions (including the typical energy output for a system, typical losses associated with shade or dust, etc.) and comparing them to other VOS studies, Dunsky undertook a three-step process. First, they identified best-practices and assumptions from similar studies. Then they adjusted variables specific to Texas. Finally, they quantified the value of solar using an avoided-cost approach, which is the minimum value that utilities would need to pay solar owners based on the value difference between purchasing energy from the solar owner compared to purchasing the energy from another source, or generating the electricity with the utility’s own generators. Based on their model, Dunsky estimates the value of solar between 2025 and 2050 to average $0.24/kWh (2024 USD).

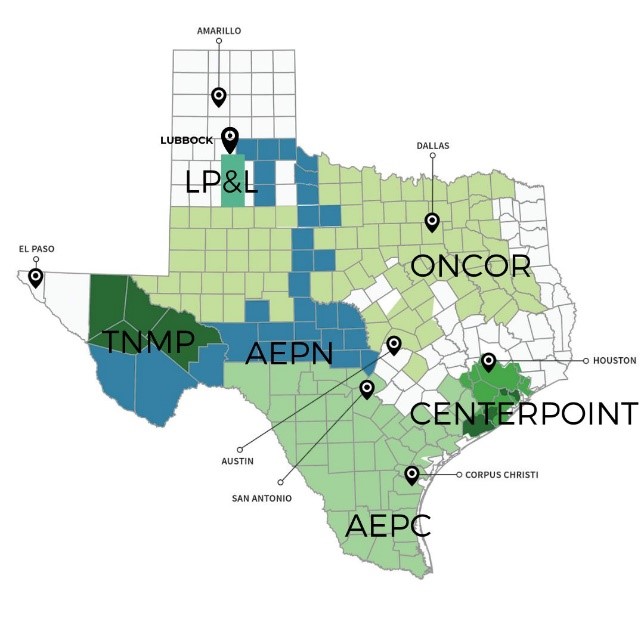

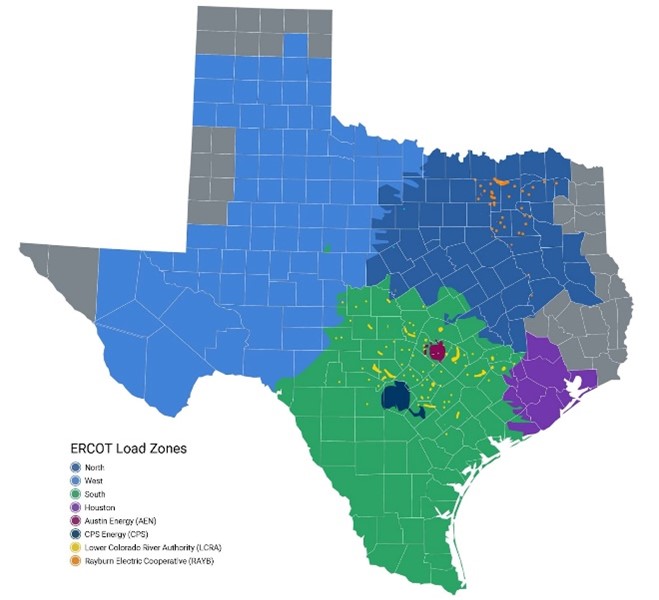

Unfortunately, there’s no available estimate of the typical solar buyback (payment plan) rate across Texas. That’s in part thanks to differing pricing mechanisms and unique details associated with each buyback plan. Fortunately, Quick Energy maintains a list of retail electric providers (private electric utilities in Texas’ deregulated markets) in Texas that offer buyback plans. By calculating the mean of average kWh prices paid to solar owners at an assumed 1000 kWh output, the typical solar owner in the Oncor transmission and distribution utility (the deregulated market in Texas centered around Dallas, where the power lines are owned and operated by Oncor) service area, is paid roughly $0.17/kWh (2024 USD). The next challenge is that the Dunsky study, unlike Quick Energy’s average buyback plans, are not based on TDU service areas, but ERCOT Load Zones (regions of the state where electric buses are parked to monitor changing electricity prices). Luckily, the North Load Zone aligns fairly close with the Oncor service area around the Dallas/North Texas region. While far from a perfect comparison, it’s an assumption based on limited information.

For 2025, Dunsky estimates the value of solar in the North Load Zone at $0.32/kWh (fairly close to other state’s estimates, such as Maine’s estimate of $0.35/kWh). Assuming a 3% rate of inflation from 2024 to 2025, Oncor’s $0.17/kWh rises to $0.18/kWh (2024 USD) in 2025. Therefore, taking the difference between $0.32/kWh and $0.18/kWh gives us the difference between the current value and the true value of solar – $0.14/kWh in 2025 (2024 USD), 78% greater than their current typical buyback rate.

There are further assumptions however that impact these numbers. The majority of retail electric providers (private utilities) have no solar buyback plan at all. The ‘typical’ solar owner may be earning much less because this back-of-envelope calculation doesn’t include those utilities without plans. Further, Quick Energy’s estimates rely on their own set of assumptions. Only one utility in the Oncor TDU pays even close to the true VOS. Chariot’s 2024 Rise 36 plan was estimated by Quick Energy to pay $0.25/kWh ($0.26/kWh in 2025), meaning it would still be $0.06/kWh away from the true VOS. Additionally, the true Rise 36 rate is more complicated than the average. The actual plan pays $0.17/kWh (retail rate) minus transmission fees but is only available to solar owners who “generate less energy than what they use, on average.”

Regardless of the intricacies of generalizing across many specific buyback plans, one thing is for certain. Texas solar owners are getting paid significantly less than what they’re worth (around 14 cents per kWh to be exact), and that’s bad for the economy and the energy industry alike. In fact, Texas is one of only two states in the country with no statewide buyback plan for solar (whether that be net metering, the method of solar valuation historically favored by solar owners, or some other value structure). In Native Solar’s words, “the lack of official state net metering policies, paired with Texas’ peculiar electricity market, makes it somewhat difficult for solar owners to navigate what solar buyback options are available to them”. If Texas wants to maintain its place in the top 10 of distributed-solar-producing states, it will have to address the underpayment of solar owners, sooner, rather than later.

——————-

Note: Maps sourced from Quick Energy and ERCOT.

Disclosure: Native Solar is a Silver Business Member of the Texas Solar Energy Society but played no part in the writing of this newsletter.

Transmission towers and lines at sunset in East Texas (Credit: Matthew T Rader, MatthewTRader.com, License CC-BY-SA)

By Ethan Miller

Back in October, I wrote an article arguing that many of last summer’s electric reliability scares and energy price increases were not the fault of renewables (as ERCOT had claimed), but the fault of insufficient transmission capacity. As it turns out, that exact problem has been generating attention around the Capitol. On Tuesday, April 30th, PowerHouse Texas hosted an Energy Innovation Forum on “Transmission in Texas,” featuring UT Webber Institute Research Scientist Dr. Joshua Rhodes. In his presentation, Dr. Rhodes highlighted Competitive Renewable Energy Zones (CREZ) for their role in increasing Texas’ transmission capacity between 2005 and 2014. One of the main takeaways was the idea that policymakers in the legislature were interested in expanding transmission capacity by pursuing a sort-of “CREZ II;” but what exactly was CREZ, how did it work, was it effective, and why is it necessary now?

Overview of CREZ

First, an overview of electricity transmission and CREZ is in order. Transmission lines are the large, metal power lines that you see. They bring electricity from generators to substations (and sometimes large industrial consumers) via direct current. Distribution lines are the smaller power lines, which carry electricity from the substations to the home via alternating current. In Texas, transmission lines are owned and operated by entities known as Transmission Service Providers (TSPs). TSPs neither own the generators, nor are they the utility that sells you end-product electricity; they exclusively operate the power lines. TSPs are overseen by ERCOT, Texas’ electric grid operator, which serves 90% of the state. ERCOT and TSPs jointly oversee some 53,000 miles of transmission lines.

In 2005, in response to increasing costs associated with transmission, SB 20 was passed to direct the Public Utility Commission of Texas (PUCT), the government entity that oversees ERCOT, to identify zones with high wind-energy potential for the construction of new transmission lines between these regions and consumer markets. The general idea behind the plan was that increasing the generating capacity of wind energy (which is ranked early along merit order – meaning it is cheapest for consumers because of its low operational costs) while simultaneously increasing grid capacity and distributing costs among all ratepayers (PowerUp Texas notes that the typical ratepayer only paid 3% more on their electric bill for CREZ wire costs), would result in an effective and efficient buildout. It appears that they were largely right. The program started with initial studies in 2006, and eight years later in 2014, the last CREZ line went into operation. The completed project added some 23 GW of additional wind generation and built-out 23% of all US high-voltage transmission in the last 12 years. The project had been projected at $4.9B, but went $2B over-budget.

Second, we need to know how CREZ worked. In 2014, ERCOT and the Department of Energy produced an overview of the program. The process began with the PUCT opening a docket to which it invited TSPs and others to make recommendations for zones, show their investment capacity, and pitch transmission line designs. The PUCT then selected zones for further study on wind capacity potential to decide ultimately whether those transmission lines would be built. After that the PUCT assigned the zones and lines to the TSPs. Along the way, PUCT staff worked with TSPs and landowners living within the proposed route to offer testimony and studies on the feasibility, costs, and roadblocks to implementation, modifying routes as necessary.

Was CREZ Successful?

The third question is whether CREZ was successful. I turn to the findings of a recent study published in the Energies journal by Heesun Jang. The study points out that after CREZ’s competition, curtailment of wind fell from 17% to 1.2%, and wholesale electric prices fell to a historic low of $24.62/MWh in 2016. The study also found that prices converged across the state (meaning the cost of a MWh of electricity was roughly comparable whether in El Paso or, Houston, etc.). Using semi-parametric regressions, Jang verified that price convergence, and decreases in prices and pollutants (in Houston in particular) from the pre-period were partially attributable to CREZ. Jang concluded that “the results show that compared with the prices in the pre-period, the prices in the post-period are lower and less volatile, especially during the high demand hours.” Jang’s findings aren’t a one-off, and are corroborated by other studies (Du & Rubin’s 2018 study in The Energy Journal and Janovska & Cohn’s research paper for Rice’s Baker Institute). Interestingly, both Jang and Jankovska & Cohn find evidence against a common point of opposition to CREZ. Critics argue that CREZ’s insistence on increasing renewable generation results in greater price variance as a result of intermittency (it’s not always windy/sunny). Jang notes that this was not significantly observed in part because CREZ created associated mitigations in congestion pricing (which increased market competition, and reduced noncompetitive strategies that generators were previously engaging in).

Jankovska & Cohn note that while CREZ did not increase the capacity of battery storage (which would increase direct dispatchability of individual generators), by connecting various, geographically dispersed generators to customer markets, there was some de-risking to the market as a whole (similar to how virtual power plants and distributed energy resources work). For example, if there is less wind in West Texas (Jang points out that 89% of wind energy is produced there) at any point, that reduced supply could be offset with Gulf-Coast wind generation (where 11% of wind is produced). Jang also notes that while the focus of CREZ is on renewables, its benefit is not confined to renewables. While CREZ lines did result in a decrease in generation from coal plants, generation from natural gas production actually increased. CREZ lines themselves are also by definition open-access lines, meaning they don’t selectively serve wind generators.

Is a CREZ II Necessary?

Most obviously, congestion pricing is an increasing challenge. The reality is that generators are overproducing electricity, but there’s insufficient transmission capacity, which is resulting in curtailment as grid operators move to avoid frying lines. These curtailment periods result in economic losses for the generators, transmission and distribution utilities, and ratepayers (who have to pay a premium to start-up peaker plants—high-cost, high-emission power plants that can provide supplemental energy to a grid during high demand—to offset the reduction in load. In ERCOT and Potomac Economics’ 2022 State of the Market Report, they note that real-time congestion costs grew 37% from 2021 at a cost of $2.8B in 2022. Researchers at Grid Strategies (Richard Doying, Michael Goggin, Abby Sherman) also report that from 2016 to 2021, total congestion costs in ERCOT grew from $497M to $2.1B, a 322.54% increase in just five years. Beyond this, building out transmission is also a necessity to meet long-term demand, as the state’s energy demand is expected to grow over time. There’s also the “forgone benefits” argument. Dr. Rhodes estimates that even building out 2/3 of the amount of transmission that the original CREZ produced would save the state $20B between 2024 and 2040. He also estimates that investing in these zones would confer $20B in local taxes, and $20B in landowner payments for leasing over the duration of the generation sources’ lifetimes. PowerUp Texas notes that these revenues will particularly benefit rural areas of the state, which are in disproportionate need of economic investment.

It is thus clear that there is an imminent need for CREZ II. Curtailment is an increasing issue, and greater transmission will be needed to meet long-term demand. The original CREZ brought together various stakeholders (including regulators, TSPs, and landowners) to collaborate and build out one of the most successful transmission programs in the entire country. CREZ also increased the generating capacity of renewables, while reducing consumer costs. In the end, a CREZ II is a no-brainer. The only concern is that generators that benefit from scarcity pricing will oppose building out transmission capacity. We must ensure that our transmission system reflects the needs of customers and all Texans alike. Through CREZ II, we can.

Disclosure: Ethan Miller is an employee of both the Texas Solar Energy Society and the Texas Climate and Energy Caucus (PowerHouse Texas’ 501c4 sister organization).

As part of the Solar Energy Innovation Network (SEIN) Round 3 program, a diverse group of energy stakeholders in Texas set out to develop and pilot new pathways to increase rooftop solar adoption to low income households. The vision: deploy rooftop solar to households owned or rented by low-income families at no cost by pairing funds from utility energy efficiency programs and other federal, state, or local government funding.

Ethan Miller, TXSES Research Associate – Policy and Government Affairs

One might think that after several years of recurrent issues with the stability of the electric grid, Texas would have established a standard system for valuing the cost of grid failures. Unfortunately, that is not the case. However, the Texas Solar Energy Society is proud to announce that it has begun the daunting task of estimating the cost of grid service interruptions to the Texas economy. Based on preliminary information from some municipal utilities, electric cooperatives, a handful of investor-owned utilities and generating retail electric providers, TXSES estimates service interruptions cost Texas at least $2B in losses in 2023. When complete, this data can be used to budget for grid reforms, save ratepayers money and increase grid reliability. To get an idea of what the final project will resemble, check out Local Solar for All’s The Economic Impact of Michigan’s Unreliable Power Grid.

TXSES calculates these costs using the Interruption Cost Estimate (ICE) calculator from Lawrence Berkeley Labs, Nexant, and the US Department of Energy. The ICE Calculator accounts for the direct costs of interruption (electricity that is generated that doesn’t hit the grid, etc.), as well as indirect costs based on FEMA formulas (cost of expired food, forgone work hours/business meetings, etc.). For the calculator to work properly, it needs measures of reliability like SAIDI (System Average Interruption Frequency Index); SAIFI (System Average Interruption Duration Index), and CAIDI (Customer Average Interruption Duration Index) scores, as well as customer counts, both residential and nonresidential. There is a maximum limit to the number of customers that can be run at one time using the calculator, so analysis has to be at a smaller scale. TXSES is using the scale of utilities (municipal utilities, co-ops, investor-owned utilities, and generating retail electric providers).

Currently, TXSES has acquired and compiled available data from the Energy Information Administration (EIA), the Public Utility Commission of Texas (PUCT), and Public Citizen. The EIA-861 forms report data from some municipal utilities and co-ops but the forms are limited in reporting on competitive markets. PUCT Dockets #54467 and #46735 provide SAIFI and SAIDI for some investor-owned utilities, but do not break down residential/nonresidential customer counts and are currently unusable. Public Citizen provides a list of all municipal utilities and co-ops in the state. While TXSES has neither complete data for the regulated nor unregulated markets, TXSES has a fuller view of data gaps within the regulated market. This is to say that while the current cost estimate is usable, it is far from complete and very likely a massive undervalue of full costs.

As TXSES continues working on this effort, be sure to follow along. Please reach out to Ethan Miller, at ethan@txses.org if you have any questions or are looking to get involved.

Sunnova’s goal is to be the source of clean, affordable, and reliable energy with a simple mission: To power energy independence so that homeowners and businesses have the freedom to live life uninterrupted®.

Founded in Houston, Texas in 2012, Sunnova started its journey to create a better energy service at a better price. Driven by the changing energy landscape, technology advancements, and demand for a cleaner, more sustainable future, we are proud to help pioneer the energy transition.

As a leading energy service provider, we help make clean, renewable energy more accessible, reliable, and affordable.

We are looking for talented and motivated individuals who thrive in a fast-paced, continuous improvement environment and want to change the world of energy. We believe in excellence in customer service and strive to ensure every customer has a reliable and optimized solar system.