By Joshua D. Rhodes, Ph.D. , Research Associate, Webber Energy Group University of Texas/Austin

There is not much in this world that has not been touched by this pandemic. Most news feeds and social media streams seem to be about the same thing: COVID, COVID and more COVID. But then again, it has touched all aspects of our lives from how we eat, to how we meet and where we put up our feet. Its impact is also being felt in the solar industry.

A recent survey by the Global Solar Council of hundreds of solar companies in dozens of countries found that more than 70% of solar companies have experienced slowdowns and about 80% expect more slowdowns in the next four months. The main reasons include supply chain interruptions, labor issues and clients being more cautious. In some regions, rooftop PV was not seen to be an “essential service” and thus was stopped altogether.

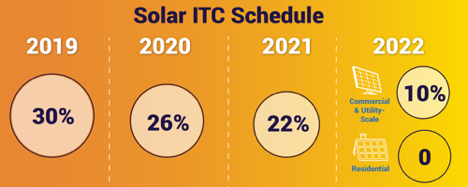

Here at home, this is a particularly challenging time for solar deployments as we are in the middle of a phase out of the Investment Tax Credit (ITC) in 2021. The rules are different for large, utility-scale and residential projects.

For example, if a utility-scale project started construction in 2019, it can – as long as construction is complete by 2024 – claim the full 30% ITC. However, residential projects are given credits based on their completion date. If the slowdown pushes a homeowner’s installation from 2020 to 2021, they receive 4% less of a tax credit. If the project is pushed out to 2022, they get zero tax credit.

There has been some discussion at the federal level about tax credit extensions for renewable energy projects, but these are likely to be most helpful to wind, perhaps retroactive, and more focused on large scale projects.

Update: the US Treasury has extended the tax credit deadline for projects to 2021, which should give developers more time to complete their projects.

COVID19 has also impacted how we use electricity. Total electricity usage is down across most of the world, including the U.S., but it is not equal across all sectors.

Industrial and commercial usage is generally down, but residential usage is up and looking different. Lower overall electricity usage could drive down wholesale electricity market prices making it less attractive to build new power plants of any type. However, solar often being the lowest cost resource, might fare better.

All of our energy systems are interrelated and connected. You can’t talk about one without talking about the others as well. The current one-two punch in the global oil markets from COVID19-driven reduced demand (i.e., we’re not traveling) and the Saudi-Russia price war has driven down the price of oil to record lows. Prices have been low before, but this time is different.

Over the past decade, the U.S. has become a major oil producer again. As low prices impact the economy, U.S. firms feel the pain. Additionally, a major portion of our domestic natural gas production is associated with oil extraction.

If we stop extracting oil, the supply of natural gas could fall, raising its price. If the price of natural gas rises, this will push up the cost of electricity because we still get almost 40% of our electricity from natural gas.

That said, if electricity prices rise, solar’s low cost will make it look even better, but this also holds true for coal. While natural gas has done the lion’s share of killing coal, higher prices could slow its march.

Most people who can have been working from home, and this has changed how we are using electricity. Most companies have been forced to put in place the infrastructure to allow their employees to work from home, even if they were previously resistant to it.

It is yet to be determined how many people will continue to work from home as a result of COVID-19, but assuming more of us will, it will be instructive to watch electricity prices, consumption and solar trends.

Joshua D. Rhodes, Ph.D. is Research Associate, Webber Energy Group University of Texas/Austin, Founding Partner, IdeaSmiths LLC and TXSES Board Member

By Ron Zagarri, North Texas Renewable Energy Group (NTREG)

June 2020

Pssst! I have a great investment opportunity for you. How would you like to get in on the ground floor of my new business? The business is capital intensive; we need to build huge factories to make our product. The product also requires significant recurring investments to keep current with our competitors – we have a lot of them – who make essentially the same product that they constantly improve. Oh yes, we also need to continually cut our prices because those annoying competitors keep lowering theirs. Interested? Hello? Anybody?

If you thought this was a crazy investment premise, you would be in good company. Yet, this is precisely what is occurring in solar module manufacturing. China has cornered the bulk of the market with secular investments in massive factories that serve global demand. Dominated by a dozen or so vertically integrated goliaths, they watch the price per watt of their solar modules decline year after year.

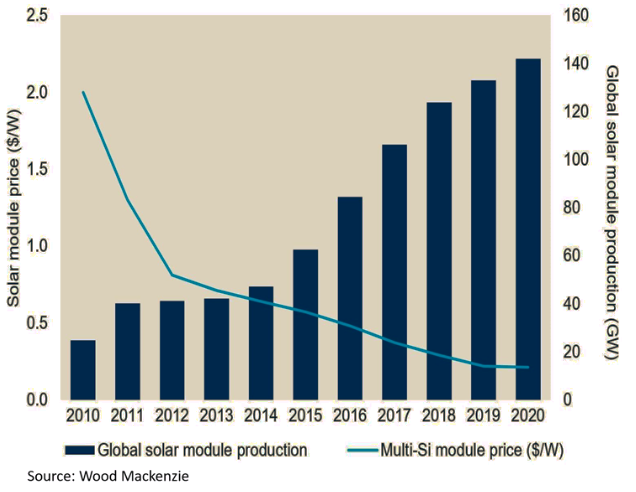

Lucky for us, price drops are not a recent phenomenon; they are down 99 percent in the last four decades. Modules cost $2 per watt in 2010, dropping to 18 cents today. In this past decade, while no other power generation technology could match this cost reduction pace, annual solar installations grew more than six-fold globally.

Let me emphasize that these are spot prices – the initial cost of a solar module at the factory gate. The wholesale cost of a module purchased in the United States is significantly higher due to tariffs, shipping, and other distribution levies. Spot prices are an important, closely watched indicator and U.S. prices inevitably follow spot price trends.

What exactly is the fundamental cause of these stunning price declines? While a major success story for renewable energy, the reasons remain elusive. One wonders if the big solar module makers are just not interested in turning a profit. Have they fixed their altruistic attention exclusively to saving the planet with inexhaustible, clean solar energy at thinner and thinner margins? Call me a cynic, but I do not believe that is happening, and the answer lies elsewhere.

Technology and Scale

With questions like this, it is always best to examine the role of technology for the answer. Creative new production techniques and technology breakthroughs often disrupt time-honored, incumbent manufacturing paradigms. Have we seen such a technological step change in solar modules in the last forty years?

Not really.

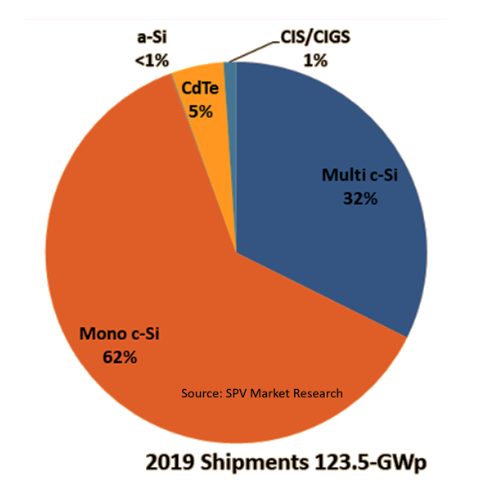

Crystalline silicon (c-Si) remains the dominant chemistry that accounts for a whopping 94 percent of the global market. A factory worker just awakening from a twenty-year coma would not observe much different in the various process steps leading from raw material to finished product today. The factory manager would welcome her back to her old job and she would quickly become a productive employee again.

There certainly have been incremental improvements in solar cell and panel efficiency, squeezing more electricity out of available sunlight. These slow and gradual refinements, also fueled by the power of Swanson’s Law, add up over time and enable lower prices. Yet, these factors account for only a portion of the module-level cost savings the industry has realized.

Others have posed this same question and examined the technology-level(“low-level”) factors that affect cost. While these bottom-up scholarly analyses are informative, low-level mechanisms dealing with the physical products themselves often miss the bigger picture shaped by economics and psychology.

Competition and Market Share

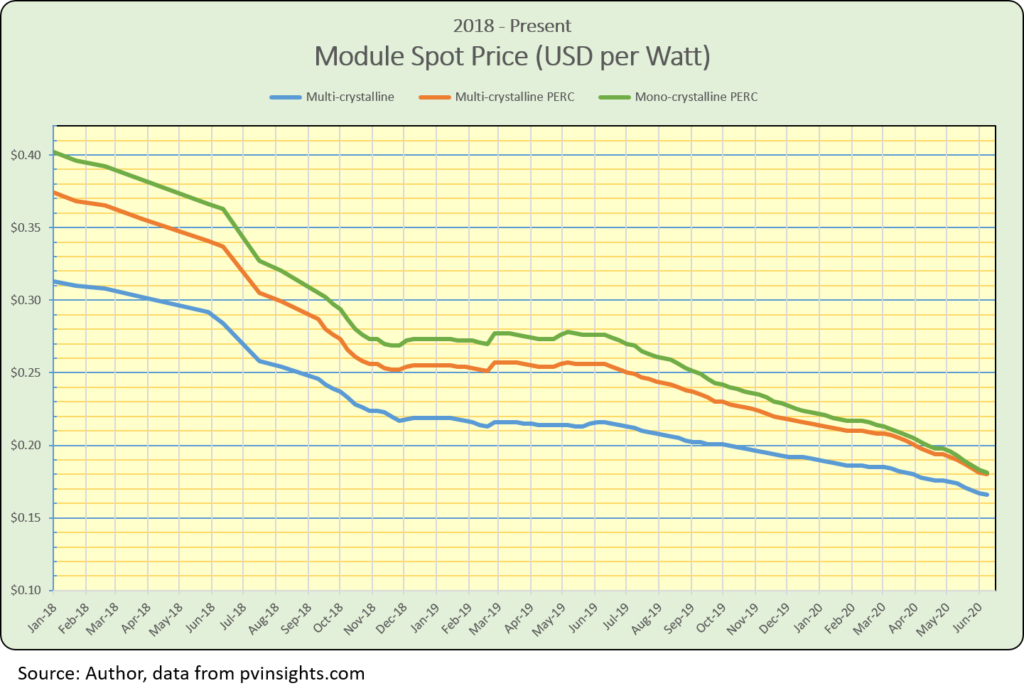

As the graph above illustrates, the cost of high-efficiency mono-crystalline PERC modules is converging to the cost of lower-efficiency module types like multi-crystalline and multi-crystalline PERC. (You are probably sorry you asked, but PERC stands for passivated emitter, rear contact, a process step that improves a solar cell’s efficiency.) A transition decades in the making, mono-crystalline has become the dominant module type over multi-crystalline, triggering a price war for market share.

Contention among the major Chinese manufacturers to be Number One and not be left behind in the capacity to produce the most popular types of modules spawns a persistent state of oversupply. The Chinese corporate chieftains, supported and encouraged by the central government, place great value in owning the largest factories, operating production lines at high throughput, and keeping employment levels elevated. This robust mass production, in excess of even the most optimistic forecasts of likely demand for the next few years, positions the fortunate buyer to demand ever-lower prices.

Meanwhile, the pandemic is a highly visible, recent market factor suppressing global demand. Rising module inventories have reinforced concerns of a slowdown in solar project activity, at least through the end of this year. Nonetheless, some Chinese producers appear ready to resume capacity expansions, as the feeling predominates that the coronavirus outbreak in China is contained.

Economics 101 – good old supply and demand – suggests that as long as manufacturers continue to over-expand and over-produce, competing for a greater share of the global market and far outpacing the market’s appetite for more solar, prices will continue on a downward trajectory. The longer this supply/demand imbalance persists, and the more time Swanson’s Law works its magic, the further solar will consolidate its position as our dominant new energy source, and the more we will witness the relentless retirements of coal and gas power plants.

How Low Can Module Prices Go?

Making cost predictions over any timeframe is a dicey game, but using the past decade as a handy portent ($2 to 18 cents), in several years we could be celebrating the spot price of solar modules falling to a nickel per watt. Oh Happy Day.

There are no inherent limits to further reductions. The industry has captured only a portion of the ultimate efficiency of c-Si solar cells, the Shockley–Queisser limit. The fixed cost of solar technology will continue to follow its version of the Moore’s Law of integrated circuits down the cost curve while forever coupled with the near-zero marginal cost of energy from the sun.

We have come such a long way to a point where it is difficult to imagine a world in which these stark economic factors could somehow fail to drive the global proliferation of ever-more renewable energy.

Ron Zagarri serves on the board of the North Texas Renewable Energy Group (NTREG) and is the past vice-chair of the Texas Solar Energy Society. He continues to volunteer with TXSES on financial and accounting matters.

In these unprecedented times when things are changing around us at incredible speed, we believe kinship is more important than ever. Staying in touch, especially now, strengthens bonds with each other and deepens our connection with community.

Despite the disruption caused by COVID-19, TXSES will continue what we’ve done for more than four decades: develop quality materials to educate Texas communities and inform decision-makers on the critical importance of sound, favorable solar policies that will grow the industry; protect clean air; build healthy, resilient communities; support local, well-paying jobs; and lay the foundation for energy independence.

Observing good social distance practices, we’re exploring ways to expand our educational outreach that reflect current and future solar trends, challenges, and opportunities via webinars, social media, and video conference calls. Have ideas you want to share? Let us hear from you! Email me at pparsons@txses.net with your suggestions.

To stay connected, we’re aggressively increasing our social media presence. If you haven’t already, like us on Facebook and follow us on Twitter. We’re also updating our website with current local, state, and national solar news and information.

We’ve rescheduled our renowned Cool House Tour to September 27, 2020. Find details about last year’s Tour here. We give profound thanks to Austin Energy’s Green Building Program for sponsoring the Tour for the past 24 years.

I want to extend heartfelt thanks for all you do to build a strong solar foundation and clean energy future for Texas, one community at a time. We stand together while apart.

Wishing health and safety for you and your loved ones.